Siemens Healthcare

Executive Summary

Siemens Healthcare Division has enjoyed large profit margins on life saving devices and capital equipment purchases over the past 20 years. That environment is rapidly changing as Moore and Metcalf’s laws drive down the technical barriers to entry and drive up the importance of connectivity.

Increasingly, medical functionality is encapsulated into broad hardware platforms like the iPad and smartphones. To drive value, the big three device firms (Siemens, GE, and Philips) are moving away from devices and towards analytics and system design, delivered through consulting and other services.

Siemens and the Medical Device Sub-Industry

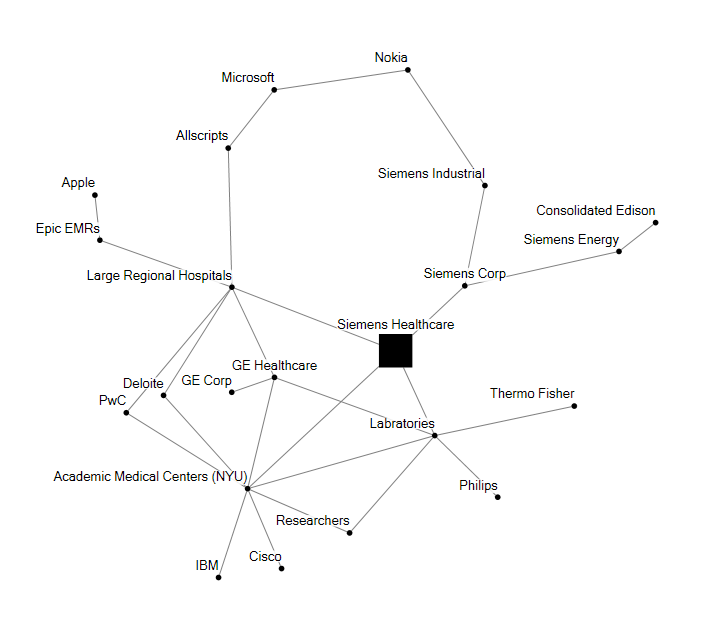

Siemens Healthcare is one of three divisions of Siemens AG, which includes an Energy division and a broad Industrial division with many business units. The Healthcare group provides imaging systems, laboratory diagnostics, therapeutics products, IT services, consulting and analytics.

Three conglomerate companies with health specific divisions dominate the electro-medical device and equipment sector: Philips, Siemens, and GE. They have traditionally benefited from large margins on major capital equipment purchases at Hospitals and Academic medical centers. Any new patient device product (ie heart sensor) or equipment procedure (ie CAT scan) is dependent on FDA approval and insurance coding. These checkpoints slow the rate of adoption and transformation in healthcare technology, but create large lock in and customer loyalty to the big three.

The combined effects of Moore and Metcalfe’s laws have created three prescient trends for the medical device industry.

- Medical functionality encapsulated into broad hardware platforms

- Commoditization of smaller and cheaper medical devices

- Integration and analytics as the key driver of value

Given these trends, the big three see competitive pressure from companies as diverse as Nike and Lockheed Martin (wearable sensors and secure system consulting). The FDA regulates traditional devices and the software they host, while applications available on the Android and Apple app store have no official scrutiny. This presents a time to market advantage in separating diagnostic and diagnose functions, which should lead to a plethora of patient centric applications in the next five years (unless the FDA begins regulating software more heavily).

New products in this market include ultrasound attachments that cost less than $1000, along with blood sugar monitors that connect to laptops or mobile devices. It has taken three years for these products to enter the market (typically they need two weeks to develop and 2.5 years to get FDA approval) since the introduction of the iPhone. Siemens recently introduced a new hearing aid app, but for the most part has divested from software investments and small-scale device products.

Siemens Healthcare Division has enjoyed large profit margins on life saving devices and capital equipment purchases over the past 20 years. That environment is rapidly changing as Moore and Metcalf’s laws drive down the technical barriers to entry and drive up the importance of connectivity.

Increasingly, medical functionality is encapsulated into broad hardware platforms like the iPad and smartphones. To drive value, the big three device firms (Siemens, GE, and Philips) are moving away from devices and towards analytics and system design, delivered through consulting and other services.

Siemens and the Medical Device Sub-Industry

Siemens Healthcare is one of three divisions of Siemens AG, which includes an Energy division and a broad Industrial division with many business units. The Healthcare group provides imaging systems, laboratory diagnostics, therapeutics products, IT services, consulting and analytics.

Three conglomerate companies with health specific divisions dominate the electro-medical device and equipment sector: Philips, Siemens, and GE. They have traditionally benefited from large margins on major capital equipment purchases at Hospitals and Academic medical centers. Any new patient device product (ie heart sensor) or equipment procedure (ie CAT scan) is dependent on FDA approval and insurance coding. These checkpoints slow the rate of adoption and transformation in healthcare technology, but create large lock in and customer loyalty to the big three.

The combined effects of Moore and Metcalfe’s laws have created three prescient trends for the medical device industry.

- Medical functionality encapsulated into broad hardware platforms

- Commoditization of smaller and cheaper medical devices

- Integration and analytics as the key driver of value

Given these trends, the big three see competitive pressure from companies as diverse as Nike and Lockheed Martin (wearable sensors and secure system consulting). The FDA regulates traditional devices and the software they host, while applications available on the Android and Apple app store have no official scrutiny. This presents a time to market advantage in separating diagnostic and diagnose functions, which should lead to a plethora of patient centric applications in the next five years (unless the FDA begins regulating software more heavily).

New products in this market include ultrasound attachments that cost less than $1000, along with blood sugar monitors that connect to laptops or mobile devices. It has taken three years for these products to enter the market (typically they need two weeks to develop and 2.5 years to get FDA approval) since the introduction of the iPhone. Siemens recently introduced a new hearing aid app, but for the most part has divested from software investments and small-scale device products.